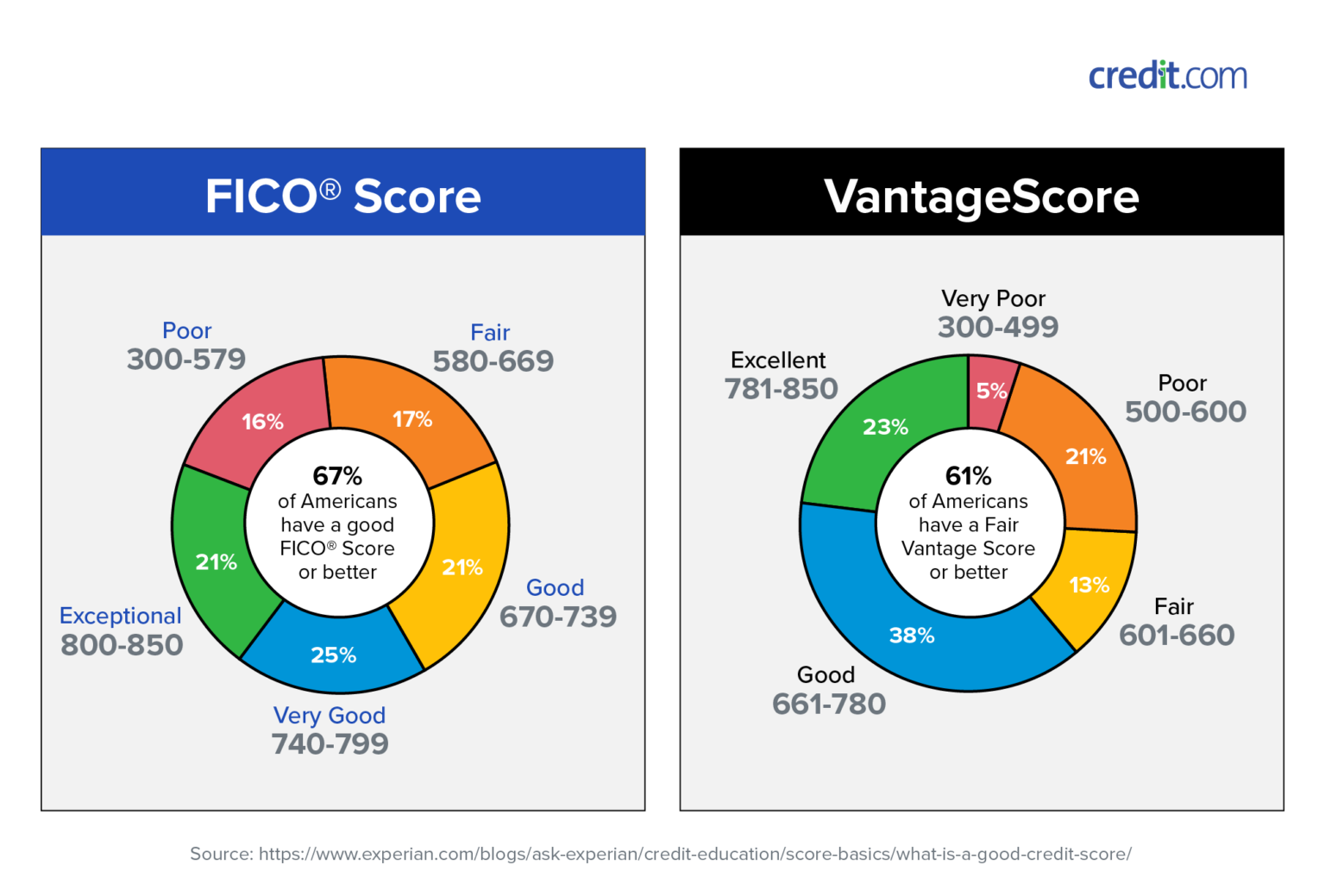

Credit scoring is a approach of figuring out the chance that credit end users will spend their charges. Truthful, Isaac started its operate with credit scoring in the late nineteen fifties and, given that then, scoring has turn out to be broadly accepted by loan companies as a trustworthy indicates of credit evaluation. A credit rating attempts to condense a borrower’s credit historical past into a solitary number. Fair, Isaac & Co. and the credit bureaus do not reveal how these scores are computed. The Federal Trade Commission has ruled this to be appropriate.

Isn’t it interesting that the score most essential in our financial lives, our customer credit score does not even incorporate full disclosure? As mentioned earlier mentioned the Federal Trade Commission has dominated that it is alright for Honest Isaac & Co not to disclose the algorithms employed in this approach, but what about buyer rights. Even though it is essential to realize what a FICO rating is, it is not the principal concern of this paper, insurance coverage costs are. So the place is the link? All the community is aware is that Truthful Isaac tells us there is a large correlation among people with undesirable credit and substantial chance motorists. This idea is crazy and from what I can see from this black box method, there is no real causation among the two. This sort of reasoning is related to convicting a man or woman of one thing just before they have even committed a crime. For instance, let’s say I do a review and that review shows there is a higher correlation in between criminals and folks with bad credit. Is this to say that just because you have poor credit you are far more most likely to commit a criminal offense and therefore you should be profiled or probably locked up since you are a danger to society?

This system is discriminating from minorities, disabled and in my scenario school pupils amid others. Reasonable Isaac & Co promises that they can not display the advanced algorithms they use to determine these correlations and scores due to the fact they worry that they would be giving up beneficial proprietary info that was really high priced to develop and sustain. What about the cost to consumer’s who may be paying greater prices or in worse instances even denied insurance based mostly on these practices.

The Equal Credit Possibility Act forbids lenders from considering race, intercourse, marital position, national origin, and religion, but if we really do not even know how these companies are calculating these scores, how in the planet could we potentially know whether or not or not they are discriminating. This smoke and mirror method is what numerous authorities businesses do to subtly discriminate and extort cash from the American.

What about extortion? As I reflect on this topic extortion will come to thoughts. Webster defines extortion as to “obtain by pressure or compulsion.” By using this sort of unfounded methods customers are forced into paying out the increased charges. 1st of all, 90% of all insurance policy companies use this process secondly in the desire of modern society legislation requires all People in america with autos to have car insurance policies. Residing in a region where it is nearly not possible to reside without having a vehicle doesn’t this current some force to pay out the charges? Also, báo cáo tài chính doanh nghiệp say you cannot find the money for to purchase a auto with funds, in which case you could acquire liability insurance policies by yourself and help save fairly a lot of cash but instead you get out a bank loan, the bank will require you to receive entire protection car insurance policy to include them till you shell out off the loan. Although this scenario may not depict an intense circumstance of extortion it does give cause to ponder the connection.

Insurance firms tout them selves as representing peace of mind, protection and stability, but at what price. In excess of the previous ten a long time, I have spent roughly twenty,000 pounds in vehicle insurance, what have I claimed? Easily considerably less than 50 % and I totaled a automobile. Is insurance coverage just a kind of legalized gambling safeguarded by federal government? The McCarran-Ferguson Act of 1944 exempts the insurance coverage industry from antitrust rules, so below we are again without having a decision collusion is the rule not competitiveness. The place are the ethics of lawmakers? Many states are screaming about this controversial issue and some states such as California have had some accomplishment, but with safety from best govt what can customers do?

I have individually written the Governor of Pennsylvania about the subject matter, a single of my principal questions was

“I am a worried citizen. Lately I discovered my automobile insurance costs increasing at a sizeable rate. I investigated the predicament only to discover out that my credit score was making the big difference, not my driving document.”

The reaction I received from the Office of Insurance policies follows:

This letter is in reponse to your complaint filed with the Pennsylvania Insurance Dpartment by means of Governor Edward G. Rendell's correspondence office relating to the use of credit as an underwriting device for automobile insurance coverage in Pennsylvania.

I have study via your issues and it appears that you are questioning the underwriting of automobile insurance policy. Especially, the use of credit in identifying eligibility. Several various factors go into the underwriting of an insurance policies policy, this sort of as sort of car, motorists, place, and many others. and most just lately credit background. Pennsylvania regulation does not prohibit an insurance policies organization fromusing credit as an underwriting instrument so lengthy as it is completed within the 1st sixty days of creating a policy. Underneath the regulation, an insurance firm is granted a 60 day window from the inception of a plan to determine no matter whether or not the plan suits into the firm's tips.

In your letter, you mentioned credit scoring in portion of the score structure and presumable must be approved by the Insurance coverage Department. In fact, credit scoring is element of a company's underwriting guidelines and the Dapartment only regulates underwriting guideline to the extent they are not discriminatory.

Also, Federal law underneath the Fair Credit Reporting Act allows credit data to be utilised for underwriting economic and insurance policy transactions.